Most business owners think a CPA will “fix everything” when finances go wrong. That belief is dangerous. A CPA can correct reports, handle taxes, and give advice, but many financial problems start inside the business long before an accountant sees them. As a result, some mistakes become too deep to fix with accounting alone.

In this guide, you will learn the most important financial mistakes business owners make, including common accounting mistakes small businesses often face, and why CPAs cannot solve them on their own. This article is created with insights inspired by Reckenen, a professional accounting and advisory firm that helps businesses improve financial clarity and long-term decision-making.

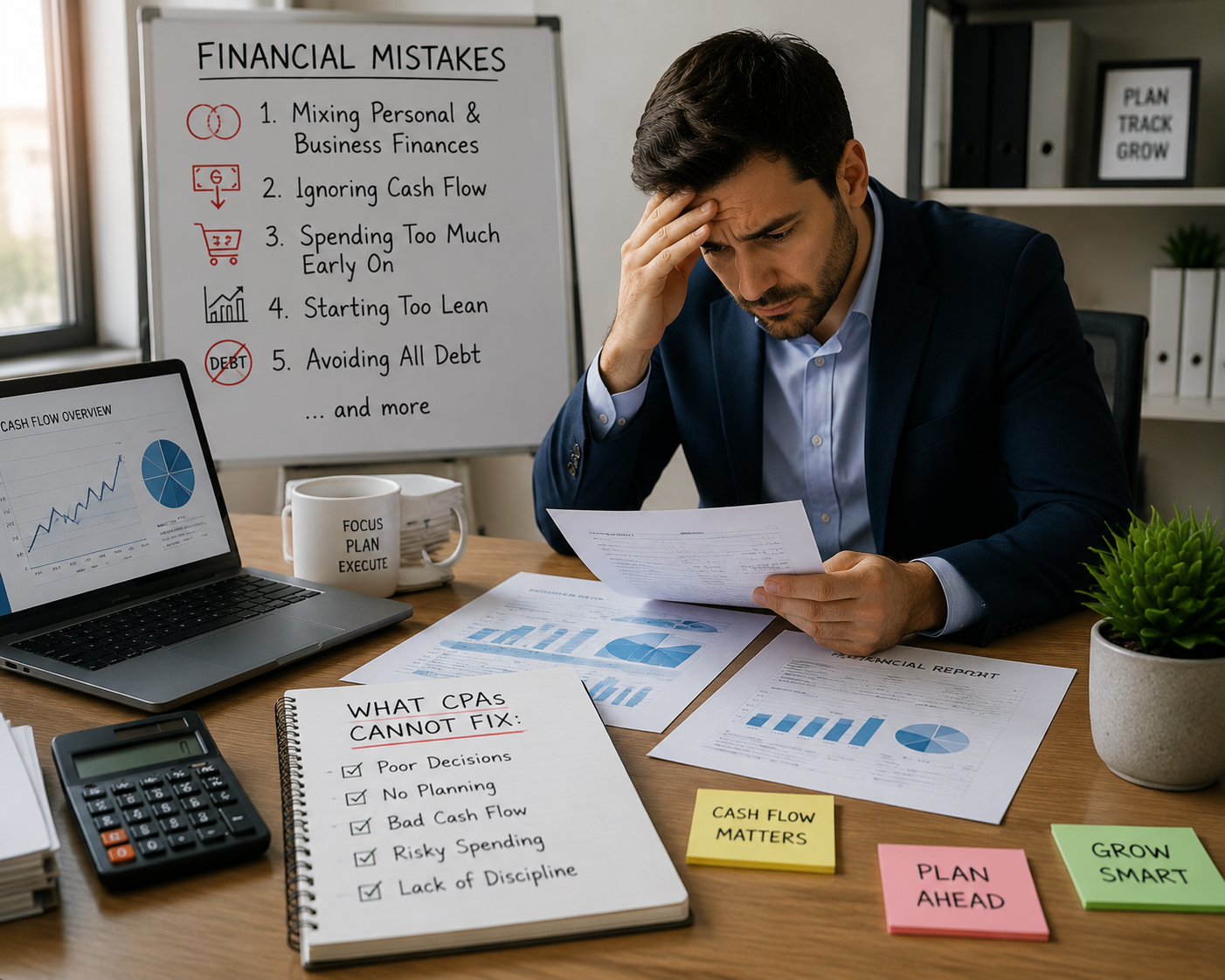

1. Mixing personal and business finances

One of the most common and damaging financial mistakes is mixing personal and business money. When business owners use the same account for both, it becomes impossible to see the real financial picture. As a result, expenses get mixed, profits become unclear, and reports lose accuracy.

Because of this confusion, CPAs cannot properly separate business performance from personal spending habits. Therefore, tax filing becomes more complex, and the risk of errors or audits increases. In simple terms, unclear money flow creates unclear business decisions.

2. Ignoring cash flow

Cash flow shows how money moves in and out of a business every day. Many businesses look profitable on paper, but still fail because they run out of cash. This happens when incoming payments are delayed, but expenses continue.

Since CPAs usually work with past financial records, they cannot control daily cash flow problems. Therefore, business owners must actively monitor cash flow to avoid financial stress. Without proper cash flow planning, even a profitable business can collapse quickly.

3. Spending too much early on

Many new businesses spend heavily in the beginning on office space, branding, equipment, and marketing. While some investment is necessary, overspending too early creates financial pressure.

As a result, the business may run out of cash before it even stabilizes. CPAs cannot undo these spending decisions once the money is gone. That is why early-stage budgeting is critical for survival.

4. Starting too lean

On the other hand, some businesses avoid spending enough. They delay hiring staff, skip important tools, and avoid proper systems to save money.

Because of this, daily operations become slow and unorganized. Growth also becomes difficult because the business lacks capacity. CPAs can highlight this weakness in reports, but they cannot fix operational underinvestment.

5. Avoiding all debt

Many business owners believe debt is always harmful, so they avoid it completely. However, not all debt is bad when used wisely for growth.

As a result of avoiding debt, businesses may miss opportunities like expansion, better inventory, or new hiring. CPAs can advise on financial structure, but they cannot make financing decisions for the business owner.

6. Not creating an emergency fund

An emergency fund acts as a financial safety net during unexpected situations like equipment failure, legal issues, or market slowdown.

Without this buffer, businesses depend on loans or credit to survive sudden problems. Therefore, CPAs cannot protect a business from financial shocks if no reserve fund exists. Planning ahead is the only real solution here.

7. Failing to plan for the unexpected

Many business owners focus only on current operations and ignore future risks such as inflation, supply chain delays, or customer loss.

Because of this lack of planning, businesses often struggle during sudden changes. CPAs can analyze what went wrong after the fact, but they cannot prevent the crisis itself. Risk planning must come from the business strategy.

8. Poor inventory management

Inventory control is critical for product-based businesses. Poor management leads to overstocking or understocking issues.

As a result, money gets stuck in unused stock, or sales are lost due to a shortage. CPAs do not manage inventory daily, so they cannot fix operational inefficiencies in real time.

9. Getting payroll wrong

Payroll mistakes directly affect employees and the business reputation. Late salaries or incorrect payments create distrust and legal risks.

Therefore, even though CPAs can correct payroll records later, they cannot repair damaged employee relationships or morale. Payroll must be handled with accuracy and consistency.

10. Skimping on insurance

Some businesses try to reduce costs by avoiding proper insurance coverage. However, this decision increases risk significantly.

Because of this, a single accident, lawsuit, or disaster can lead to major financial loss. CPAs cannot recover lost assets or reverse such damage after it happens.

11. Missing tax deadlines or deductions

Late tax filing leads to penalties, interest, and compliance issues. Many businesses also miss legal deductions due to poor planning.

Although CPAs help with tax preparation, they cannot remove penalties caused by delays or missing information. Timely planning is always the responsibility of the business.

12. Overlooking business credit

Business credit is important for loans, financing, and vendor relationships. When owners ignore it, they limit future financial opportunities.

As a result, growth becomes harder because access to funding is restricted. CPAs can guide credit strategy, but they cannot build credit history instantly.

13. Not investing profits for growth

Many businesses keep profits unused instead of reinvesting them into expansion, marketing, or better systems.

Because of this, competitors move ahead faster while the business stays stagnant. CPAs can suggest investment options, but the final growth decision always depends on the business owner.

FAQs:

1. Can a CPA fix all financial problems in a business?

No, a CPA cannot fix all financial problems. They can correct records, manage taxes, and give advice, but they cannot change poor spending habits, cash flow decisions, or business strategies made by owners.

2. Why do businesses still fail even with a CPA?

Businesses fail because many problems start at the operational level. For example, poor cash flow, overspending, or lack of planning cannot be fully solved by accounting alone.

3. What is the most dangerous financial mistake in a business?

Mixing personal and business finances is one of the most dangerous mistakes. It creates confusion in records, affects tax accuracy, and hides the real profit of the business.

4. How can business owners reduce financial mistakes?

Business owners can reduce mistakes by tracking cash flow, keeping separate accounts, planning budgets, managing risks, and reviewing financial reports regularly.

5. When should a business seek help from a CPA?

A business should hire or consult a CPA when financial records become complex, taxes need proper handling, or when professional advice is needed for compliance and long-term planning.

Why Financial Discipline Matters More Than Fixes

CPAs play an important role in every business, but they are not miracle fixers. They work with the data you give them, not the decisions you make in real time. Therefore, strong financial discipline inside the business is the real foundation of long-term success.

When business owners control spending, track cash flow, plan ahead, and manage risk properly, they reduce financial pressure on accountants and improve overall performance. In the end, a CPA can support growth, but only a well-managed business can truly achieve it.

Grow your business with clear financial guidance from Reckenen today.