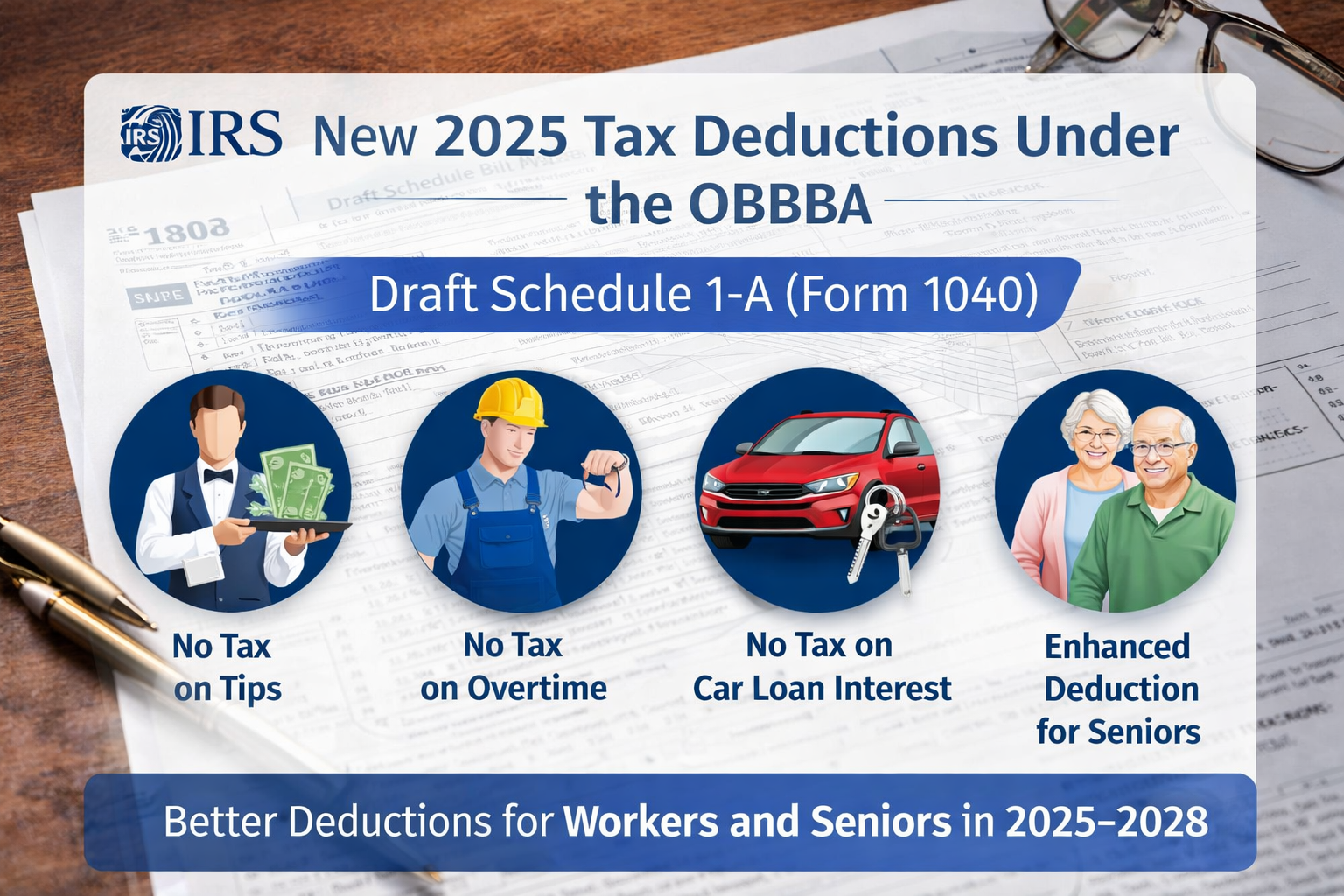

The IRS has released a draft of Schedule 1-A (Form 1040), introducing a new reporting structure for several deductions created under the One Big Beautiful Bill Act (OBBBA). These new tax deductions — available from 2025 through 2028 — are designed to provide targeted relief for workers and seniors.

The draft form represents one of the first major implementation steps for the new law and outlines how taxpayers will claim deductions for:

- Tips

- Overtime pay

- Car loan interest

- An enhanced deduction for seniors

If you’re planning ahead for the 2025 tax year, understanding how these provisions work could create meaningful tax planning opportunities.

What Is Schedule 1-A (Form 1040)?

Schedule 1-A is a newly proposed IRS form that consolidates several OBBBA deductions into one reporting schedule. These deductions are classified as “below-the-line” deductions, meaning:

- They reduce taxable income

- They do not reduce Adjusted Gross Income (AGI)

- They can be claimed whether or not you itemize deductions

While marketed as “no tax” provisions, these are technically income deductions, not exclusions. Taxpayers must still report income properly — the deduction simply lowers taxable income subject to federal tax.

Breakdown of the Four New 2025–2028 Tax Deductions

1. No Tax on Tips Deduction (2025–2028)

This deduction benefits service industry workers who receive reported tips.

Who Qualifies?

Employees receiving qualified tips reported on:

- Form W-2

- Form 1099-NEC

- Form 1099-MISC

- Form 1099-K

Deduction Limit

Up to $25,000 per filer

Income Phaseout Begins At:

- $150,000 Modified Adjusted Gross Income (MAGI) for single filers

- $300,000 MAGI for married filing jointly

Additional Requirements

- Valid Social Security number

- Married taxpayers must file jointly

Example

A server reporting $20,000 in qualified tips could deduct that amount, subject to income phaseout limits.

SEO keywords: no tax on tips deduction 2025, tip income tax deduction, OBBBA tips deduction

2. No Tax on Overtime Deduction

Designed to benefit hourly workers, this provision allows a deduction for qualified overtime pay.

Who Qualifies?

Wage earners receiving federally required overtime compensation under the Fair Labor Standards Act (FLSA).

Only the additional “half” portion of time-and-a-half pay qualifies.

Deduction Limit

- $12,500 per filer

- $25,000 for joint filers

Income Phaseout Begins At:

- $150,000 MAGI (single)

- $300,000 MAGI (joint)

Important Limitation

State-specific overtime rules do not qualify — only federally mandated overtime applies.

Example

An eligible employee with $10,000 in qualified overtime earnings may deduct that amount, subject to phaseout rules.

SEO keywords: overtime tax deduction 2025, no tax on overtime OBBBA, FLSA overtime deduction

3. No Tax on Car Loan Interest Deduction

This new deduction allows taxpayers to deduct interest paid on certain new vehicle purchases.

Who Qualifies?

Taxpayers who:

- Purchased a new personal-use vehicle after December 31, 2024

- The vehicle is assembled in the United States

- Has a gross vehicle weight rating under 14,000 pounds

- The purchase is secured by a loan lien

Deduction Limit

Up to $10,000 per filer for interest paid

Income Phaseout Begins At:

- $100,000 MAGI (single)

- $200,000 MAGI (joint)

Exclusions

- Used vehicles

- Leased vehicles

- Business-use vehicle loans

Example

A married couple paying $6,500 in interest on a qualified auto loan with MAGI below $200,000 could deduct the full $6,500.

SEO keywords: car loan interest deduction 2025, auto loan tax deduction OBBBA, new vehicle tax deduction

4. Enhanced Deduction for Seniors (Age 65+)

The OBBBA also provides additional tax relief for retirees.

Who Qualifies?

Individuals age 65 and older with valid Social Security numbers. Married taxpayers must file jointly.

Deduction Amount

- $6,000 per filer

- $12,000 for joint filers

Income Phaseout Begins At:

- $75,000 MAGI (single)

- $150,000 MAGI (joint)

Example

A retired couple with $120,000 in MAGI may qualify for most of the enhanced deduction before phaseout reduces the benefit.

SEO keywords: senior tax deduction 2025, enhanced deduction age 65, retiree tax relief OBBBA

Important Planning Considerations for 2025

Although these provisions are branded as “no tax” measures, they:

- Do not eliminate income reporting requirements

- Do not reduce AGI

- Are subject to income-based phaseouts

- Are temporary (2025–2028 only)

The IRS is expected to release final instructions clarifying documentation requirements and calculation methods before the 2025 filing season.

Because these deductions are temporary, strategic timing of income, vehicle purchases, and retirement distributions may be especially important during the 2025–2028 window.

What This Means for Tax Planning

The introduction of Schedule 1-A signals a structural change in how individual tax deductions will be reported beginning in 2025.

Workers who earn significant tips or overtime, individuals planning to purchase a vehicle, and retirees over age 65 should begin evaluating how these changes could impact taxable income projections.

At Reckenen, we monitor legislative developments and IRS implementation guidance to help clients plan proactively — not reactively. Early analysis can help maximize available deductions while avoiding unintended phaseout limitations.

If you’d like guidance on how the new 2025 tax deductions under the OBBBA may apply to your specific situation, our team is available to help you build a forward-looking tax strategy.